Tax compliance is important in Singapore. Every individual is required to file a personal tax return every calendar year regardless of resident or non-resident status, on all his/ her incomes including gains or profits from a trade or earnings from employment. Foreign sources of income of a Singapore tax resident are exempt from income tax except for the income received through a partnership in Singapore.

If a tax resident’s annual income is $22,000 or more, filing a personal tax return is mandatory. Tax residents do not need to pay tax if the annual income is less than $22,000. However, you might still be required by The Inland Revenue Authority of Singapore (IRAS) to file a tax return if you have been informed by IRAS to do so as tax compliance is taken seriously in Singapore.

You are a tax resident if you meet one of the following tax compliance criteria:

- A Singapore Citizen or Permanent Resident residing in Singapore except temporary absences

- A foreigner who has worked or stayed in Singapore for (excluding director of a company) for 183 days or more in the year before year of assessment

Tax Residents

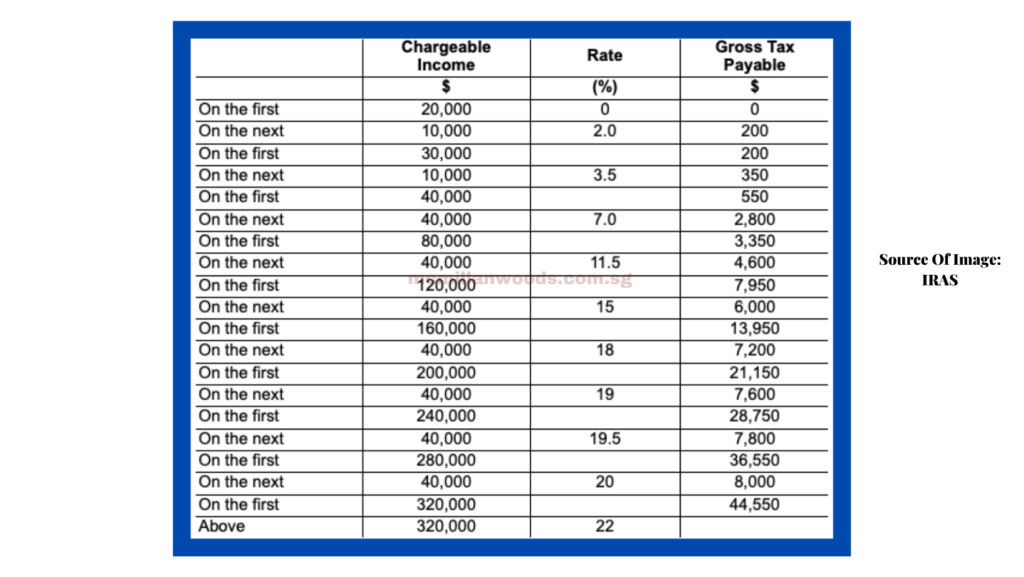

Personal income tax rate in Singapore is one of the lowest in the world and in order to determine the income tax liability of an individual, you need to first determine the tax residency and amount of chargeable income before applying the progressive resident tax rate to it.

Eg. Nothing is chargeable on the first $20,000 but 2% is chargeable on the first $10,000 after $20,000, meaning that if your income falls between the $22,000 to $30,000 ceiling, you will be required to pay $200. Tax residents in Singapore are taxed on a progressive resident tax rate as listed below.

Non-Tax Residents

Non-tax residents are exempt from income tax compliance under the following reasons:

- If the individual is in Singapore on short term employment for 60 days or less in a year. Do take note that the exemption does not apply to the director of a company, a public entertainer or exercising of a profession in Singapore

- The individual is taxed on all income earned in Singapore (no personal relief applies) at 15% or the resident rate within a period of 61 to 182 days, whichever gives rise to a higher tax amount

- Director fees, consultant fees and other incomes are taxed at 20%

Other Tax Compliances On Individuals

1. Property Tax

This is a wealth tax compliance imposed on property ownership in Singapore irrespective of whether the property is vacant or occupied. It is also applicable to Housing Development Board flats and private properties. The rates are progressive and are different for owner occupied and non-owner occupied homes. Rates are 0% to 15% for owner occupied property; 10% to 19% for non-owner occupied property and 10% for non-residential property.

2. Rental Income Tax

Income tax compliance is also imposed on investment properties, meaning rental income is taxable when it is due and payable to the property owner instead of the date of actual receipt. Rental income from the letting of property in Singapore is subject to income tax while the property itself is subject to property tax.

3. Stamp Duty

This is a tax compliance on documents related to immovable properties, stocks or shares including lease/ tenancy agreements, transfer of shares and mortgages. Once the document is signed and dated, the duty needs to be paid and this can be done easily via IRAS’s e-Stamping system.

4. Vehicle Taxes

Aside from import duties, these are taxes imposed on motor vehicles. The purpose of imposing these taxes is to control car ownership and road congestion. The taxes also include various registration fees, road taxes and special taxes etc.

5. Central Provident Fund (CPF) Contributions

These are payable to Singapore citizens and Permanent Residents only. Every company is required to pay the employer’s share of CPF contributions monthly for all applicable employees. Likewise, employees are also required to contribute their share to the CPF at a rate of 20% and graduated rates may apply for the first 3 years when the employee just obtained Permanent Residency. The employer’s statutory contribution rate to CPF is currently at 16%, subject to a monthly ordinary wage ceiling of S$5,000 and the total annual wage ceiling of S$ 85,000.

In summary, as long as you take note and file your income tax return accordingly and on time, there won’t be any penalties regarding tax compliance. The process has been made easier by IRAS’s online portal, everything can be done within 15 minutes. We hope the information has been helpful.